Secured Vs Unsecured Loans Explained

Introduction

Loans play a major role in personal and business finance by providing access to funds for various purposes. Whether an individual wants to purchase a home, finance education, cover medical expenses, or expand a business, loans can provide the necessary financial support. However, not all loans operate in the same way.

One of the most important distinctions in lending is the difference between secured loans and unsecured loans. These two categories differ in terms of collateral requirements, approval processes, interest rates, risk levels, and repayment conditions.

Understanding the differences between secured and unsecured loans helps borrowers make informed financial decisions and select loan products that align with their financial needs and repayment capabilities.

This guide explains secured and unsecured loans, their features, advantages, disadvantages, and the key factors borrowers should consider before applying.

What Is a Loan?

A loan is a financial agreement in which a lender provides money to a borrower with the expectation that the borrower will repay the amount over a specified period, usually with interest.

Loan agreements typically include:

- Loan amount

- Interest rate

- Repayment period

- Monthly payment amount

- Fees and charges

- Terms and conditions

Loans generally fall into two main categories:

- Secured loans

- Unsecured loans

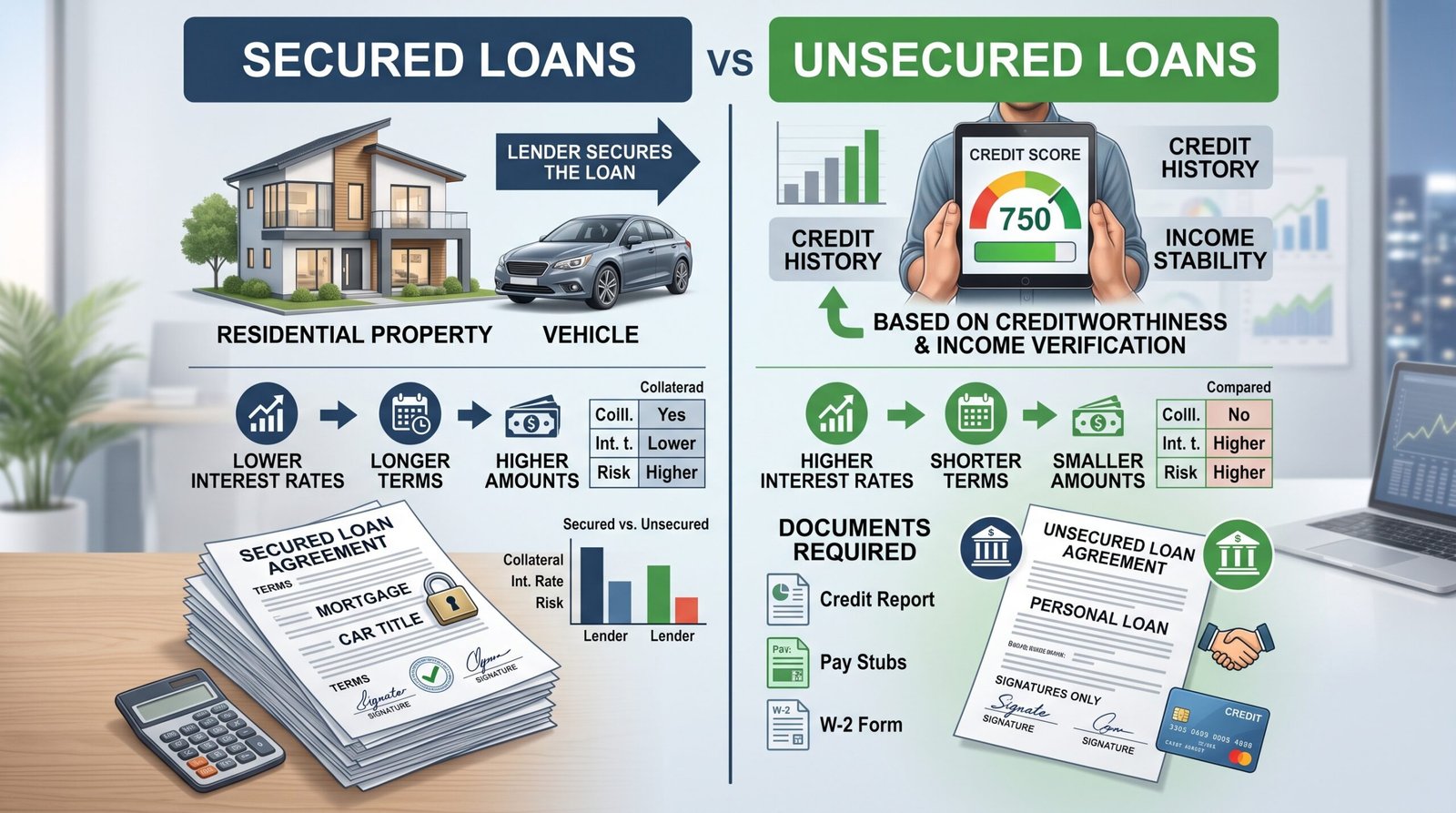

What Is a Secured Loan?

A secured loan is a type of borrowing that requires the borrower to provide collateral.

Collateral is an asset that the lender can claim if the borrower fails to repay the loan.

Common forms of collateral include:

- Real estate

- Vehicles

- Savings accounts

- Investments

- Business assets

- Equipment

Collateral reduces the lender’s financial risk.

Examples of Secured Loans

Several common financial products are secured loans.

Examples include:

Mortgage Loans

Collateral:

- Residential property

- Commercial property

Auto Loans

Collateral:

- Purchased vehicle

Home Equity Loans

Collateral:

- Home equity

Secured Personal Loans

Collateral:

- Savings accounts

- Certificates of deposit

- Other financial assets

Business Loans

Collateral:

- Equipment

- Inventory

- Property

Secured loans are widely used because they reduce lender risk.

How Secured Loans Work

The secured loan process generally follows these steps:

Step 1: Application

The borrower submits:

- Personal information

- Financial information

- Collateral details

Step 2: Collateral Evaluation

The lender evaluates:

- Asset value

- Ownership status

- Market conditions

Step 3: Credit Assessment

The lender reviews:

- Credit history

- Income

- Debt obligations

Step 4: Loan Approval

If approved, the lender issues the loan.

Step 5: Repayment

The borrower repays according to the loan agreement.

If repayment fails, the lender may seize the collateral.

Advantages of Secured Loans

Secured loans provide several benefits.

Lower Interest Rates

Because collateral reduces lender risk, secured loans often have lower interest rates.

Higher Borrowing Limits

Borrowers may qualify for larger loan amounts.

Longer Repayment Terms

Repayment periods may extend over many years.

Easier Approval

Collateral can improve approval chances, especially for borrowers with limited credit history.

Improved Loan Flexibility

Lenders may offer more favorable conditions.

These advantages make secured loans attractive for major financial needs.

Disadvantages of Secured Loans

Secured loans also involve risks.

Risk of Asset Loss

Failure to repay may result in:

- Foreclosure

- Repossession

- Asset seizure

Longer Approval Process

Collateral verification can increase processing time.

Additional Documentation

Borrowers often provide:

- Ownership documents

- Appraisals

- Insurance records

Reduced Financial Flexibility

Collateral remains tied to the loan until repayment is complete.

Borrowers should carefully evaluate these risks.

What Is an Unsecured Loan?

An unsecured loan does not require collateral.

Approval decisions are based primarily on:

- Credit history

- Income

- Employment

- Financial stability

- Debt obligations

Because no collateral exists, lenders assume greater financial risk.

Examples of Unsecured Loans

Common unsecured loan products include:

Personal Loans

Used for:

- Medical expenses

- Travel

- Home improvements

- Debt consolidation

Credit Cards

Allow revolving borrowing without collateral.

Student Loans

Many educational loans do not require collateral.

Medical Loans

Some healthcare financing options are unsecured.

Signature Loans

Approval depends primarily on borrower creditworthiness.

These loans provide flexibility without requiring assets.

How Unsecured Loans Work

The unsecured loan process generally includes:

Step 1: Application Submission

Applicants provide:

- Personal information

- Employment information

- Financial records

Step 2: Credit Evaluation

Lenders review:

- Credit scores

- Payment history

- Existing debt

Step 3: Income Verification

Income and employment are verified.

Step 4: Risk Assessment

Lenders estimate repayment risk.

Step 5: Loan Approval

Approved applicants receive funds without providing collateral.

Advantages of Unsecured Loans

Unsecured loans offer several benefits.

No Collateral Requirement

Borrowers do not risk losing personal assets.

Faster Approval Process

Applications often require less documentation.

Simpler Application Procedures

Fewer asset evaluations are required.

Greater Asset Protection

Personal property remains unaffected by the loan agreement.

Financial Flexibility

Borrowers can access funds without pledging property.

These features make unsecured loans attractive for many consumers.

Disadvantages of Unsecured Loans

Unsecured loans also have limitations.

Higher Interest Rates

Because lenders assume greater risk, interest rates are often higher.

Lower Borrowing Limits

Loan amounts may be restricted.

Stricter Approval Requirements

Lenders may require:

- Higher credit scores

- Stable employment

- Strong income history

Shorter Repayment Periods

Repayment schedules may be shorter.

Borrowers should consider these factors carefully.

Major Differences Between Secured and Unsecured Loans

Several key differences distinguish these loan types.

| Feature | Secured Loans | Unsecured Loans |

|---|---|---|

| Collateral | Required | Not Required |

| Interest Rates | Usually Lower | Usually Higher |

| Approval Difficulty | Easier | More Difficult |

| Loan Amount | Higher | Lower |

| Repayment Terms | Longer | Shorter |

| Risk to Borrower | Asset Loss | Credit Damage |

| Processing Time | Longer | Faster |

Understanding these differences helps borrowers choose appropriately.

Interest Rate Comparison

Interest rates vary significantly between loan types.

Secured Loan Rates

Interest rates may be lower because lenders have collateral protection.

Examples:

- Mortgages

- Auto loans

- Secured personal loans

Unsecured Loan Rates

Interest rates may be higher because lenders accept more risk.

Examples:

- Credit cards

- Personal loans

- Signature loans

Credit scores also influence final interest rates.

Which Loan Is Easier to Obtain?

Approval difficulty depends on several factors.

Secured Loans

Borrowers may qualify more easily because collateral reduces lender risk.

Unsecured Loans

Lenders rely heavily on:

- Credit scores

- Income

- Employment stability

Applicants with strong financial histories often qualify more easily.

Which Loan Is Safer?

The answer depends on perspective.

Borrower Perspective

Unsecured loans protect personal assets.

Lender Perspective

Secured loans reduce financial losses.

Both loan types involve different risks and benefits.

When Should You Choose a Secured Loan?

Secured loans may be suitable when:

- Large amounts are required

- Lower interest rates are desired

- Long repayment periods are needed

- Valuable collateral is available

Examples include:

- Home purchases

- Vehicle financing

- Business investments

When Should You Choose an Unsecured Loan?

Unsecured loans may be appropriate when:

- Immediate funds are required

- No collateral is available

- Smaller loan amounts are needed

- Asset protection is important

Examples include:

- Medical expenses

- Debt consolidation

- Emergency expenses

Factors to Consider Before Choosing a Loan

Before borrowing, evaluate:

Financial Goals

Determine the purpose of the loan.

Repayment Ability

Calculate monthly repayment capacity.

Interest Costs

Compare borrowing costs.

Risk Tolerance

Assess willingness to provide collateral.

Loan Terms

Review:

- Interest rates

- Fees

- Repayment schedules

- Penalties

Careful evaluation reduces financial risk.

Common Borrower Mistakes

Common mistakes include:

- Borrowing more than necessary

- Ignoring interest costs

- Failing to compare lenders

- Overlooking repayment obligations

- Using collateral carelessly

- Missing payment deadlines

Avoiding these mistakes improves financial outcomes.

Example Comparison

Suppose two borrowers need $20,000.

| Feature | Secured Loan | Unsecured Loan |

|---|---|---|

| Loan Amount | $20,000 | $20,000 |

| Interest Rate | 7% | 13% |

| Repayment Period | 5 Years | 3 Years |

| Monthly Payment | Lower | Higher |

| Collateral | Required | Not Required |

This example illustrates the trade-offs between loan types.

Conclusion

Secured and unsecured loans each serve important financial purposes. Secured loans offer lower interest rates, larger borrowing amounts, and easier approval but require collateral. Unsecured loans provide greater flexibility and asset protection but often involve higher interest rates and stricter approval requirements.

Choosing between secured and unsecured loans depends on financial goals, risk tolerance, available assets, and repayment capacity. Understanding the differences between these loan types helps borrowers make informed financial decisions and manage debt responsibly.

Frequently Asked Questions (FAQ)

What is the main difference between secured and unsecured loans?

Secured loans require collateral, while unsecured loans do not.

Are secured loans easier to obtain?

In many cases, yes, because collateral reduces lender risk.

Do unsecured loans have higher interest rates?

Yes. Unsecured loans often carry higher interest rates due to increased lender risk.

Can I lose my property with a secured loan?

Yes. Failure to repay may result in the lender claiming the collateral.

Which loan type is safer for borrowers?

Unsecured loans generally provide greater asset protection.

Can I get an unsecured loan with poor credit?

Approval may be more difficult, but some lenders offer options for borrowers with lower credit scores.

Which loan type is better?

The best choice depends on individual financial circumstances, borrowing needs, and risk tolerance.

Related Posts

Tips For Paying Off Loans Faster

How Loan Interest Rates Are Calculated