Tips For Paying Off Loans Faster

Introduction

Loans help individuals achieve financial goals such as purchasing homes, financing education, buying vehicles, starting businesses, and covering emergency expenses. However, carrying debt for extended periods can increase financial pressure and result in substantial interest costs over time.

Paying off loans faster provides several benefits, including reduced interest expenses, improved cash flow, better credit management, and increased financial freedom. While loan agreements establish minimum payment schedules, borrowers often have opportunities to accelerate repayment and reduce total borrowing costs.

This guide explains practical strategies for paying off loans faster, reducing interest expenses, and improving long-term financial stability.

Why Paying Off Loans Faster Matters

Accelerating loan repayment offers several financial advantages.

Benefits include:

- Reduced interest costs

- Faster debt elimination

- Improved credit profile

- Increased savings opportunities

- Greater financial flexibility

- Reduced financial stress

- Improved cash flow management

- Enhanced long-term financial security

Even small additional payments can significantly reduce total borrowing costs.

Understand Your Loan Details

Before creating a repayment strategy, understand the terms of your loan.

Review:

- Outstanding balance

- Interest rate

- Loan term

- Monthly payment

- Payment due dates

- Early repayment penalties

- Additional fees

Understanding your loan structure helps develop an effective repayment plan.

Create a Loan Repayment Budget

A budget provides a foundation for faster loan repayment.

Include:

- Monthly income

- Essential expenses

- Savings contributions

- Debt payments

- Discretionary spending

Example Budget

| Category | Amount |

|---|---|

| Monthly Income | $4,000 |

| Living Expenses | $2,500 |

| Savings | $300 |

| Minimum Loan Payment | $500 |

| Extra Loan Payment | $400 |

| Remaining Funds | $300 |

Allocating funds specifically for loan repayment improves consistency.

Pay More Than the Minimum Payment

One of the simplest ways to repay loans faster is to pay more than the required minimum.

For example:

| Monthly Payment Type | Amount |

|---|---|

| Minimum Payment | $300 |

| Additional Payment | $100 |

| Total Payment | $400 |

Additional payments reduce:

- Principal balance

- Interest costs

- Repayment period

Even modest increases can shorten loan terms significantly.

Make Extra Payments Regularly

Additional payments directly reduce the principal balance.

Strategies include:

- Monthly extra payments

- Quarterly lump-sum payments

- Annual bonus payments

- Tax refund payments

Reducing the principal balance decreases future interest charges.

Use the Debt Snowball Method

The debt snowball method focuses on paying smaller debts first.

Steps include:

- List debts from smallest to largest balance.

- Make minimum payments on all debts.

- Direct additional funds toward the smallest debt.

- Eliminate debts one by one.

Example

| Debt | Balance |

|---|---|

| Credit Card A | $1,000 |

| Personal Loan | $5,000 |

| Auto Loan | $15,000 |

Advantages include:

- Increased motivation

- Visible progress

- Simplified debt management

Many borrowers find this method psychologically rewarding.

Use the Debt Avalanche Method

The debt avalanche method prioritizes loans with the highest interest rates.

Steps include:

- List debts by interest rate.

- Continue minimum payments.

- Direct extra payments toward the highest-interest debt.

- Repeat until all debts are paid.

Example

| Debt | Interest Rate |

|---|---|

| Credit Card | 22% |

| Personal Loan | 12% |

| Auto Loan | 6% |

Benefits include:

- Lower total interest costs

- Faster financial savings

- Efficient debt reduction

This strategy often minimizes total borrowing expenses.

Make Biweekly Payments

Instead of making one monthly payment, consider biweekly payments.

Example:

- Monthly payment: $600

- Biweekly payment: $300 every two weeks

This approach results in:

- Twenty-six half-payments annually

- Thirteen full payments per year

Additional annual payments can shorten loan terms.

Round Up Payments

Rounding up payments creates additional principal reductions.

Example:

| Required Payment | Actual Payment |

|---|---|

| $462 | $500 |

| $675 | $700 |

Small increases accumulate over time.

This strategy is easy to implement and maintain.

Apply Windfall Income to Loans

Unexpected income provides opportunities to accelerate repayment.

Examples include:

- Tax refunds

- Bonuses

- Gifts

- Inheritance

- Freelance income

- Business profits

Applying these funds to loan balances can significantly reduce debt.

Reduce Unnecessary Expenses

Reducing discretionary spending creates additional repayment capacity.

Possible reductions include:

- Subscription services

- Entertainment expenses

- Dining expenses

- Shopping purchases

- Luxury spending

Redirecting these funds toward loans speeds repayment.

Increase Your Income

Additional income can accelerate debt reduction.

Potential income sources include:

- Freelancing

- Part-time employment

- Consulting

- Online businesses

- Rental income

- Overtime work

Higher income creates more flexibility for extra payments.

Refinance Existing Loans

Refinancing replaces an existing loan with a new loan.

Potential benefits include:

- Lower interest rates

- Lower monthly payments

- Shorter repayment periods

- Reduced total borrowing costs

Refinancing may be beneficial when:

- Credit scores improve

- Market rates decline

- Financial conditions change

Borrowers should compare costs carefully.

Consolidate Multiple Loans

Loan consolidation combines multiple debts into one loan.

Potential advantages include:

- Simplified payments

- Lower interest rates

- Improved organization

- Fixed repayment schedules

Consolidation may help borrowers manage debt more efficiently.

Avoid Taking on Additional Debt

New borrowing can slow repayment progress.

Avoid:

- Unnecessary credit card spending

- Additional personal loans

- Impulse financing

- Excessive borrowing

Focusing on existing debt improves financial outcomes.

Set Specific Repayment Goals

Establish measurable repayment objectives.

Examples include:

- Pay off $5,000 within one year

- Eliminate credit card debt within six months

- Reduce loan balance by 50% within two years

Clear goals improve motivation and accountability.

Automate Loan Payments

Automatic payments provide several benefits.

Advantages include:

- Consistent payments

- Reduced missed payments

- Better financial discipline

- Potential interest discounts

Automation supports long-term repayment success.

Track Your Progress

Monitoring progress helps maintain motivation.

Track:

- Remaining balances

- Monthly payments

- Interest savings

- Repayment timelines

Progress tracking provides visibility into financial improvements.

Avoid Prepayment Penalties

Some loans include prepayment penalties.

Before making additional payments, verify:

- Loan agreements

- Penalty clauses

- Early payoff conditions

Avoiding penalties ensures that extra payments produce maximum benefits.

Prioritize High-Interest Debt

High-interest debt often creates the greatest financial burden.

Examples include:

- Credit cards

- Payday loans

- Unsecured personal loans

Prioritizing these obligations reduces total interest costs.

Example of Accelerated Loan Repayment

Suppose:

- Loan amount: $20,000

- Interest rate: 10%

- Original term: 5 years

Standard Payment

| Monthly Payment | Loan Term |

|---|---|

| $425 | 60 Months |

Accelerated Payment

| Monthly Payment | Loan Term |

|---|---|

| $525 | Approximately 46 Months |

Additional payments reduce both repayment time and total interest costs.

Common Mistakes When Paying Off Loans

Borrowers often make avoidable mistakes.

Examples include:

- Paying only minimum amounts

- Ignoring interest rates

- Missing payment deadlines

- Taking additional debt

- Failing to create budgets

- Not comparing refinancing options

Avoiding these mistakes improves financial outcomes.

Benefits of Becoming Debt-Free

Paying off loans provides significant advantages.

Benefits include:

- Improved cash flow

- Reduced financial obligations

- Increased savings opportunities

- Better investment potential

- Reduced financial stress

- Greater financial independence

Debt freedom creates additional financial opportunities.

Conclusion

Paying off loans faster requires planning, discipline, and consistent financial habits. Strategies such as making additional payments, reducing expenses, increasing income, refinancing, and prioritizing high-interest debt can significantly reduce repayment periods and interest costs.

Successful debt repayment is not solely about earning more money; it also depends on effective financial management and commitment to long-term financial goals. By implementing practical repayment strategies, borrowers can achieve financial freedom more quickly and strengthen their overall financial health.

Frequently Asked Questions (FAQ)

Is it better to pay off loans early?

Paying off loans early often reduces total interest costs and improves financial flexibility.

What is the debt snowball method?

The debt snowball method focuses on paying off the smallest debts first.

What is the debt avalanche method?

The debt avalanche method prioritizes debts with the highest interest rates.

Can extra payments reduce loan interest?

Yes. Additional payments reduce the principal balance, which lowers future interest charges.

Should I refinance my loan?

Refinancing may help if it reduces interest rates or improves repayment terms.

Are biweekly payments effective?

Yes. Biweekly payments often reduce repayment periods and total interest costs.

What should I do if I cannot make extra payments?

Focus on budgeting, reducing expenses, and increasing income when possible.

Related Posts

How Loan Interest Rates Are Calculated

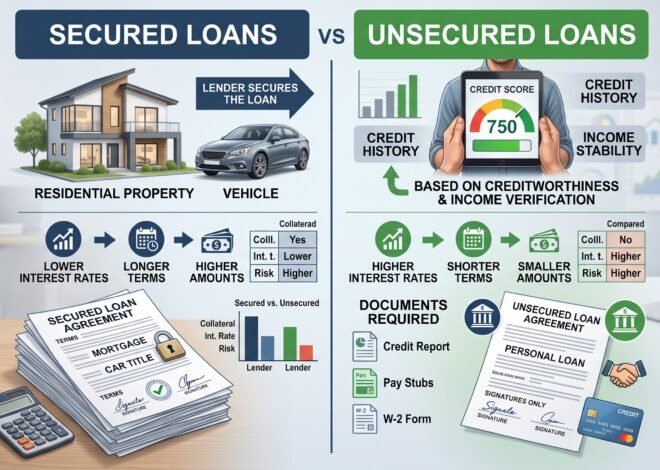

Secured Vs Unsecured Loans Explained