How Loan Interest Rates Are Calculated

Introduction

Interest rates are one of the most important components of any loan agreement. Whether an individual applies for a personal loan, mortgage, auto loan, student loan, or business loan, the interest rate determines the total cost of borrowing money.

Understanding how loan interest rates are calculated helps borrowers make informed financial decisions, compare loan offers, estimate repayment costs, and manage debt effectively. Loan interest calculations involve several factors, including the principal amount, interest rate, repayment period, credit score, and lending policies.

This guide explains how loan interest rates are calculated, the factors that affect interest rates, and the common methods lenders use to determine borrowing costs.

What Is Loan Interest?

Loan interest is the amount charged by a lender for providing money to a borrower. It represents the cost of borrowing and is usually expressed as a percentage of the loan amount.

The borrower agrees to repay:

- The original loan amount (principal)

- The interest charged by the lender

Interest allows lenders to:

- Earn profits

- Cover operating costs

- Manage lending risks

- Compensate for inflation

What Is the Principal Amount?

The principal amount is the original amount borrowed.

For example:

| Loan Type | Principal Amount |

|---|---|

| Personal Loan | $10,000 |

| Auto Loan | $25,000 |

| Mortgage | $250,000 |

Interest calculations are generally based on this principal balance.

What Is an Interest Rate?

An interest rate is the percentage charged annually on borrowed money.

Example:

- Loan amount: $10,000

- Annual interest rate: 10%

The interest rate determines how much additional money the borrower pays over time.

Interest rates may be:

- Fixed

- Variable

Fixed Interest Rates

A fixed interest rate remains unchanged throughout the loan period.

Example:

- Loan amount: $20,000

- Interest rate: 8%

- Loan term: 5 years

Benefits include:

- Predictable payments

- Stable budgeting

- Protection from market changes

Fixed rates provide certainty for borrowers.

Variable Interest Rates

Variable interest rates may change during the loan period.

These rates are often linked to:

- Market interest rates

- Central bank policies

- Financial indexes

Benefits may include:

- Lower initial rates

- Potential savings if rates decrease

Risks include:

- Payment increases

- Greater financial uncertainty

Borrowers should understand these risks before choosing variable-rate loans.

Basic Interest Calculation Formula

Simple interest is calculated using the following formula:

Interest = Principal × Rate × Time

Example:

- Principal: $5,000

- Interest rate: 10%

- Time: 2 years

Calculation:

Interest = $5,000 × 0.10 × 2

Interest = $1,000

Total repayment:

$5,000 + $1,000 = $6,000

Simple interest calculations are commonly used for short-term loans.

Compound Interest Calculation

Many loans use compound interest.

Compound interest means that interest is calculated on:

- The principal amount

- Previously accumulated interest

The compound interest formula is:

A = P(1 + r/n)^(nt)

Where:

- A = Total amount

- P = Principal

- r = Annual interest rate

- n = Number of compounding periods

- t = Time in years

Compound interest increases borrowing costs over time.

Annual Percentage Rate (APR)

Many lenders use the Annual Percentage Rate (APR).

APR includes:

- Interest charges

- Certain loan fees

- Additional borrowing costs

APR provides a broader estimate of loan costs than interest rates alone.

Example:

| Loan | Interest Rate | APR |

|---|---|---|

| Loan A | 7% | 7.8% |

| Loan B | 7% | 8.4% |

Comparing APR helps borrowers evaluate loan offers more accurately.

Factors That Affect Loan Interest Rates

Several factors influence interest rate calculations.

Credit Score

Credit scores are among the most important factors.

Higher credit scores often result in:

- Lower interest rates

- Better loan terms

Lower credit scores may lead to:

- Higher rates

- Additional requirements

Income

Lenders review:

- Income level

- Income stability

- Employment history

Higher income may reduce lending risk.

Debt-to-Income Ratio

The debt-to-income ratio measures existing debt obligations.

The formula is:

Debt-to-Income Ratio = Monthly Debt ÷ Monthly Income × 100

Lower ratios often result in better interest rates.

Loan Amount

Large loan amounts may affect:

- Risk assessments

- Interest calculations

Loan Term

Longer repayment periods often involve:

- Higher total interest costs

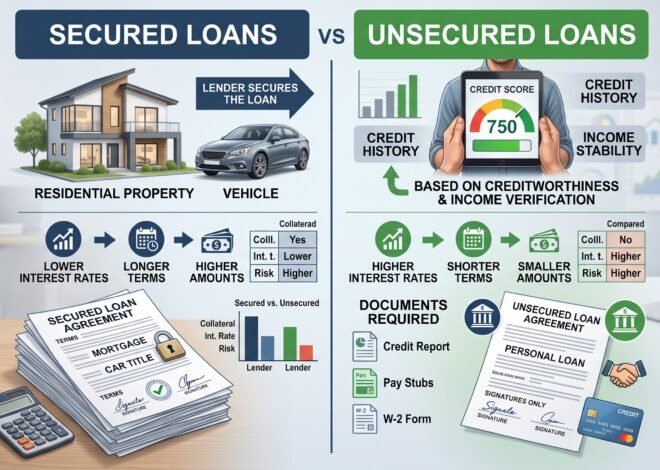

Collateral

Secured loans generally have:

- Lower interest rates

Collateral reduces lender risk.

How Credit Scores Affect Interest Rates

Credit scores directly impact borrowing costs.

Example:

| Credit Score | Possible Interest Rate |

|---|---|

| 750+ | Lower |

| 700–749 | Moderate |

| 650–699 | Higher |

| Below 650 | Highest |

Maintaining good credit can significantly reduce total borrowing costs.

How Loan Terms Affect Interest

Loan duration affects total interest payments.

Example:

Five-Year Loan

- Lower total interest period

- Higher monthly payments

Ten-Year Loan

- Higher total interest period

- Lower monthly payments

Borrowers should balance affordability and total cost.

How Mortgage Interest Is Calculated

Mortgage lenders typically use amortization schedules.

Each payment includes:

- Principal repayment

- Interest payment

During the early years:

- Interest payments are larger

Later in the loan:

- Principal payments increase

This process gradually reduces the outstanding balance.

How Personal Loan Interest Is Calculated

Personal loans commonly use:

- Simple interest

- Fixed-rate calculations

Factors affecting rates include:

- Credit score

- Income

- Loan amount

- Repayment period

Personal loan rates vary among lenders.

How Credit Card Interest Is Calculated

Credit cards generally use daily interest calculations.

The process includes:

- Determining the daily interest rate.

- Calculating average daily balances.

- Applying interest daily.

Because of frequent compounding, credit card borrowing can become expensive.

Amortization Explained

Amortization refers to the gradual repayment of debt through scheduled payments.

Each payment includes:

- Interest expense

- Principal reduction

Example:

| Payment | Interest | Principal |

|---|---|---|

| First Payment | High | Low |

| Final Payment | Low | High |

Amortization schedules help borrowers understand repayment progress.

Why Interest Rates Vary Between Borrowers

Not all borrowers receive identical rates.

Differences may result from:

- Credit history

- Income

- Employment

- Collateral

- Loan amount

- Loan purpose

- Market conditions

Lenders evaluate individual risk profiles.

How Central Banks Influence Interest Rates

Central bank policies affect lending rates.

When central banks increase rates:

- Borrowing costs often increase

When central banks reduce rates:

- Borrowing costs may decrease

Economic conditions strongly influence lending markets.

How to Reduce Loan Interest Costs

Borrowers can reduce costs through several strategies.

Improve Credit Scores

Methods include:

- Paying bills on time

- Reducing debt

- Monitoring credit reports

Compare Multiple Lenders

Shopping for loans helps identify competitive rates.

Choose Shorter Loan Terms

Shorter repayment periods often reduce total interest.

Make Additional Payments

Extra payments reduce principal balances faster.

Use Secured Loans When Appropriate

Collateral may lower interest costs.

These strategies can reduce total borrowing expenses.

Example Loan Calculation

Assume:

- Loan amount: $10,000

- Interest rate: 8%

- Loan term: 3 years

Approximate repayment:

| Item | Amount |

|---|---|

| Principal | $10,000 |

| Interest | $1,300 |

| Total Repayment | $11,300 |

Actual amounts vary based on lender calculations.

Common Borrower Mistakes

Common mistakes include:

- Ignoring APR

- Focusing only on monthly payments

- Borrowing excessive amounts

- Choosing long repayment terms unnecessarily

- Failing to compare lenders

- Overlooking fees

Avoiding these mistakes reduces financial costs.

Conclusion

Loan interest rates determine the true cost of borrowing money. Lenders calculate interest using various factors, including credit scores, income, debt levels, loan terms, and market conditions. Understanding how interest rates work helps borrowers compare loan options, estimate repayment costs, and make informed financial decisions.

By improving credit profiles, comparing lenders, and selecting appropriate loan terms, borrowers can reduce interest expenses and manage debt more effectively.

Frequently Asked Questions (FAQ)

What is loan interest?

Loan interest is the cost charged by lenders for borrowing money.

What is the difference between fixed and variable interest rates?

Fixed rates remain constant, while variable rates may change over time.

What is APR?

APR represents the annual cost of borrowing, including interest and certain fees.

How does credit score affect interest rates?

Higher credit scores often result in lower interest rates.

What is compound interest?

Compound interest is calculated on both the principal and accumulated interest.

Can I reduce my loan interest costs?

Yes. Improving credit scores, comparing lenders, and making additional payments can reduce borrowing costs.

Why do different borrowers receive different interest rates?

Lenders assess each borrower’s financial risk individually, resulting in different rates.

Related Posts

Tips For Paying Off Loans Faster

Secured Vs Unsecured Loans Explained